Should We Be Concerned About the National Debt?

As the US national debt approaches $28 trillion, the question of how this staggering amount could possibly be paid off arises. Indeed, the debt amounts to over 130% of the United States GDP and if it were to be paid off by taxpayers alone, each taxpayer would have to pay over $222,000. The deficit (the amount added to the principal every year) has more than doubled since 2015 and continues to rise due to government borrowing to provide large COVID stimulus packages. In fact, even if the deficit was reduced to zero, the national debt would still grow by hundreds of billions of dollars every year as interest accrues.

While this situation may seem dire, the national debt has been able to rise to today’s insurmountable levels without a financial doomsday event. How long can this unsustainable borrowing persist? What negative effects could arise from these continual increases in the national debt? And what solutions exist that provide hope for relief from this monumental problem?

Factors to Consider:

Low interest rates have allowed the US government to shoulder a heavier debt burden than was previously thought possible. While taking on too much debt is always going to have a negative effect no matter how low interest rates are, many see today’s ultra-low rates as an important opportunity for our government to invest in projects that will pay off in the long-term, such as infrastructure (roads, energy, widespread broadband), healthcare and education for the poor, scientific research, and projects that mitigate future environmental damages. Interest rates are projected to increase to more normal levels over the next decade or two, meaning both that the government’s current borrowing habits will have to be tempered soon and that these ideal conditions for long-term investment will recede in the near future.

Modern Monetary Theory (MMT) proposes that monetarily sovereign countries like the US which spend, tax, and borrow in a fiat currency (currency not backed by a physical commodity like gold or silver, but by the government that issues the currency) that they fully control do not need to rely on taxes or borrowing for spending since they can print as much as they need and are the monopoly issuers of the currency. Essentially, if this theory is correct, the US could simply print however much money they need to pay off the national debt. While this theory makes practical sense at first, the majority of economists reject it, stating that simply printing money would cause inflation to skyrocket. Venezuela is a good example of a country that printed money to pay off its debts and subsequently suffered from immense inflation rates. In 2014, Venezuela suffered from a very high deficit, so it printed out enough money to pay off its debts over a period of 2 years. This was enough money to quadruple their money supply. After all of this money was printed, Venezuela suffered a 60% annual inflation rate. The United States’ M2 money supply is estimated at about $19.56 trillion as of January 2021, meaning that if about $28 trillion were printed to pay off the federal debt, the M2 money supply would increase by over 140%, which would likely lead to an incredibly high inflation rate.

In order to prevent rampant deficit rises, the US Congress does impose debt ceilings, which are regulations on levels of government debt that force Congress into limiting budget deficits – unless it can agree to raise the debt ceiling. While the debt ceiling is a good way to create strict boundaries on how large the deficit can amount to, it can be raised or suspended (as it was in 2019, to free up funding for coronavirus stimulus packages; this suspension expires in July 2021).

Federal debt can eventually crowd out private borrowing if the national debt continues to grow, causing interest rates to rise. This is one of the critical ways that the national debt can affect the lives of everyday Americans as every facet of life that requires borrowing money becomes more expensive when interest rates rise. As could be inferred, reducing the national debt would prevent this phenomenon from occurring.

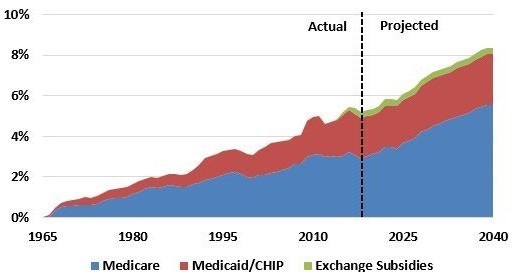

Healthcare costs are rising disproportionately more than economic growth. That is, healthcare prices are rising relative to other goods/services and relative to GDP (Figure 1 shows the government’s healthcare expenditures as a percentage of GDP over time). Because the federal government covers a large portion of the healthcare system, a significant amount of national debt increases are catalyzed by increasing healthcare costs. Indeed, the U.S. spent almost $1.2 trillion on healthcare in the fiscal year 2019, which amounts to over a third of the year’s $3.5 trillion in tax revenue. A more efficient and less costly healthcare system would certainly help combat growing federal budget deficits. Public policy changes to facilitate this, as well as innovative new technologies, are likely the key to addressing this component of the national debt.

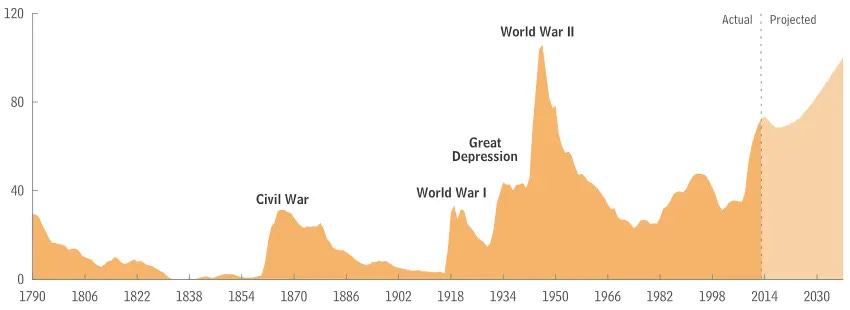

Figure 1 (Source: CRFB) Another area where the US could considerably improve with regards to debt generation is military/law enforcement spending. There is a strong positive correlation between war and national debt, as Figure 2 shows (Figure 2 shows national debt as a percentage of GDP over time). With the expensive War on Drugs having persisted for nearly a century with no success in curbing addiction, ending it is a big opportunity to reduce the deficit. In fact, legalizing all drugs could generate $46.7 billion in annual tax revenues if drugs were taxed at the same rate as alcohol and tobacco are taxed today. This is on top of the $41.1 billion in estimated annual savings from ending the War on Drugs (calculation for both of these estimates were done by Professor Jeffrey Miron of the Department of Economics at Harvard University). Political opinions aside, the United States’ continued military action in the Middle East serves as another avenue from which costs could be cut to reduce the national debt.

Figure 2 (Source: EconomicsHelp.Org) Cutting spending and/or increasing taxes to some degree are undoubtedly a necessity to lower the national debt to more sustainable levels. Because the debt far exceeds annual tax revenue, this would have to be done over a long period of time to significantly lessen the national debt. This raises valid concerns about the government’s ability to aid in future economic crises like the one we are experiencing right now, should the debt continue to persist at this unsustainable level. This risk underpins arguments for combating the debt sooner rather than later to lower the time window during which decreased spending and/or increased taxes must take place. Unfortunately, it may not be realistic to start cutting costs or raising taxes to address this problem until after the economy has stabilized from the devastating effects of the coronavirus pandemic.

Interesting discussion; several monetary theories will be tested in real time in the next few years.