Silicon Valley Bank's Full Autopsy

What Caused the Second Largest Bank Failure in United States History?

Introduction

Silicon Valley Bank (SVB) was a unique institution in the values it strove for and the customers it served, which separated its identity from other, larger banks that exist throughout the world. Established in 1983, the company developed for about 40 years before its demise. It was able to IPO in 1988 and expanded across the globe into areas such as Israel, the U.K., China, Canada, Germany, and Denmark. The bank was built to help advance innovation throughout economies. Their website pushes this message frequently with slogans such as “the financial partner of the innovation economy” and “advancing innovation for a better world” (Silicon Valley Bank, n.d.). This meant that SVB catered to a smaller and more niche clientele, mainly consisting of venture capital firms, startups, and wealthy individuals. While one can argue that it was essential that SVB existed for these clients as it provided a banker for this ecosystem, it also left the company exposed to the ebbs and flows of the startup and venture capital world. More so, without proper risk management, potential downturns or stress would expose the bank to failure as risks materialized. As discussed below, the fall of SVB revealed systematic risks that all banks face; however, the individual characteristics of the company’s clients, assets, and liabilities caused the second-largest bank failure since the fall of Washington Mutual Bank in 2008, as shown in Figure 1. To dig into this, several areas will be examined, such as the regulatory environment, the effects of COVID-19, accounting designations, the macroeconomic landscape, inadequate risk management, a concentrated funding base, weakening profitability, and government intervention.

Importance of Regulation on SVB’s Frame

The regulatory stature in the background of SVB’s failure serves as an excellent explanation of why the company could operate the way that it did. The most crucial regulation for the bank came in the form of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) installed during the financial crisis in 2008 via the Obama administration. This law was a flight toward regulation in the wake of fear and banking contagion spreading throughout the economy at the time. Dodd-Frank heavily regulated the financial industry and prevented it from making riskier investments that could expose its capital to more significant losses in the future. While covering the bill would take up too much space and time, it is summarized quite nicely by Niall Ferguson in his book The Ascent of Money as he writes:

Dodd-Frank was a near perfect example of excessive complexity in regulation. The Act required that regulators create 243 rules, conduct 67 studies and issue 22 periodic reports. It eliminated one regulator and created two new ones. By 2014, according to one estimate, the total number of new restrictions associated with Dodd-Frank (27,669) exceeded the restrictions generated by all the other legislation passed under the Obama administration. (Ferguson, 2008)

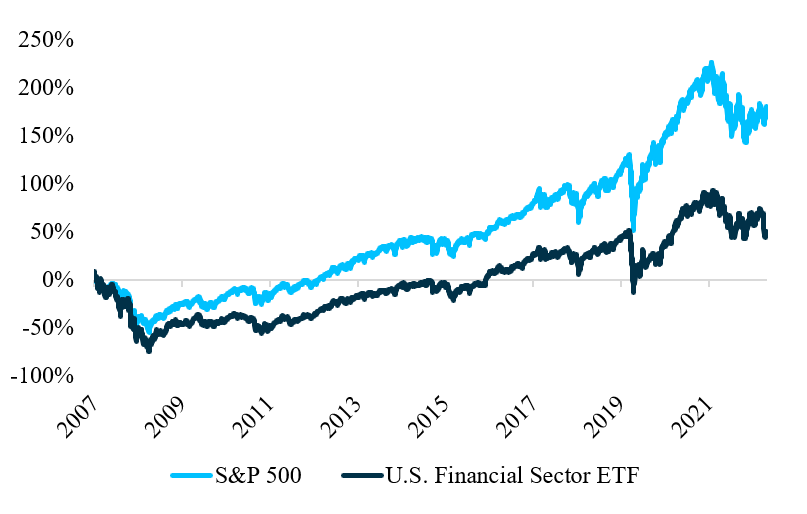

Some would argue that it was because of increased regulation like the Dodd-Frank Act that banks became less competitive as an investment causing their growth and innovation to slow. This is suggested by comparing the financial sector to the overall market since 2008 in percentage appreciation terms, as shown in Figure 2. However, this is a discussion for another time.

The importance of the Dodd-Frank Act concerning SVB comes with a rule implemented upon the Act’s inception. Specifically, it required banks with more than $50 billion in assets to take annual stress tests given by the Federal Reserve. These tests would examine a bank’s balance sheet and ability to stay liquid or solvent in the event of an economic contraction of varying levels. The Act also created the Financial Stability Oversight Council (FSOC) and the Consumer Financial Protection Bureau (CFPB), which oversaw the supervision of the Act. While SVB would have been subject to these tests in 2008, the bank never had to conduct them due to legislation changes in 2018 under the Trump administration. The Reduced Regulatory Burdens for All but the Largest Bank Holding Companies Act eliminated the need “for bank holding companies with less than $250 billion in assets to comply with most aspects of the ‘enhanced prudential standards,’ including resolution planning, stress testing, and single-counterparty credit limits” (The Harvard Law School Forum on Corporate Governance, 2018). If one examines the size of SVB’s assets before failure, curious enough, it was right under the threshold at $212 billion. In effect, legislation changes in 2018 removed the need for SVB to conduct stress tests as extensive as the larger banks in the U.S. are required to do, along with having more relaxed supervisory on the health of its balance sheet. This regulatory frame allowed SVB to take on more hidden, individual risks that supervisors missed before its downfall. As discussed in the next section, these risks were only enhanced as COVID-19 stimulus introduced trillions of dollars of liquidity into the system.

The Effects of COVID-19

Around $5 trillion was given to different sectors of the economy over COVID-19 times; such areas included households, restaurants, airlines, hospitals, local governments, and other institutions. More importantly for the topic of SVB was that businesses received $1.7 trillion, and “more than nine million small businesses – generally those with 500 employees or fewer – collected loans through the Paycheck Protection Program (PPP)” (Parlapiano et al., 2022). Needless to say, a ton of money flooded the system, with many businesses and individuals flush with cash. More so, front and long-end rates were dropped from lowering the federal funds rate and quantitative easing. This allowed for cheap money, which boosted the stock market, and even more so boosted the size and quantity of equity offerings that SVB’s clients could complete. Due to this, one can see a massive increase in the bank’s deposits post-pandemic as most of these startups needed to place their newly acquired dry powder somewhere. To increase this funding, SVB sometimes required startups to hold most of their cash with the bank for it to conduct business with them. For example, “CNBC has reviewed six agreements that companies signed with SVB regarding financing or credit solutions. All required the companies to open or maintain bank accounts with SVB and use the firm for all or most of their banking services” (Goswami, 2023). In simple terms, to gain a loan from SVB, a company would need to hold their cash there as well, most likely forcing an even greater amount of deposits to flow into the bank, as shown in Figure 3.

As these deposits came into SVB, the bank realized that the opportunity to loan was diminishing compared to the vast amount of funding it received. More so, because the bank operated in such a niche sector, its knowledge of whom to loan to was more concentrated, further narrowing the options. For instance, when looking at SVB’s loan book, one can see just how focused it was on the technology and venture capital sectors, as shown in Figure 4.

Rather than push to invest in startups or firms they felt would not give the desired return, SVB decided to park the funds from depositors in ultra-safe assets. However, while one may think there should be no issue with doing so, it comes down to the specific characteristics of the assets they invested in and the macro environment that affected them, which will be discussed in the following sections.

The Importance of Accounting

SVB’s strategy of piling funds into safe assets such as Treasuries or Agency asset-backed securities (ABS) was common for banks following the 2008 financial crisis. Due to increased regulation, as discussed earlier, banks must also hold a certain amount of high-quality liquid assets (HQLA) on their balance sheet. The number of HQLAs banks buy is dictated by their Liquidity Coverage Ratio (LCR), which has to maintain a level above 100%. The LCR measures whether the bank can meet stressed outflows of deposits for 30 days or more. Calculating the LCR is simply the stock of HQLA the bank holds divided by the net cash outflow over 30 days, equaling greater than 100% . Of course, Treasuries and Agency ABS meet the criteria for HQLA due to the high liquidity and low credit risk associated with these securities (both are usually rated AA to AAA). However, even though the perceived risk of these securities is low, the way that SVB handled investing in them exposes idiosyncratic risks the institution took.

SVB’s latest 10-K shows that by the end of 2022, the bank had a massive bond portfolio valued at nearly $120 billion. One can see this increase in Figure 3 as securities increased along with deposits. Comparing these bonds against all the bank’s assets, it was a staggering 57% compared to an industry average of 24%, as shown in Figure 5. This had several implications for the bank’s profitability as these long-term fixed assets decreased in value as interest rates rose, as discussed in a later section. While other banks may hold fixed securities, they will also have a more considerable amount of loans that usually have a floating rate which will adjust to a rising rate environment, keeping profitability stable.

It is crucial to break down this bond portfolio to understand it better. Accounting is prominent in how this portfolio is laid out on the company’s financial statements. There are two distinct categories that the securities purchased can be placed into. The first is Available for Sale (AFS), meaning the company purchased these investments to sell them later in the future. The accounting treatment of AFS securities considers the fair market value as time goes on and will record unrealized gains or losses that will affect the company’s asset and equity values depending on the change. The second is Held to Maturity (HTM), meaning the company purchased these securities to hold them until maturity. The accounting treatment of HTM securities differs from AFS in that the investments' fair market value is not considered when showing the value of assets and equity as time progresses. Instead, the HTM category is kept at book value with no fluctuations taken into account, with a separate category describing any unrealized gain or losses that investors can view. However, these unrealized changes are nonimportant due to the nature of HTM, as the securities already have a set amount of return and value that will be realized once they expire. With these two distinctions, SVB could separate its bond portfolio into each category and disguise any changes under the larger HTM section. Investors never seemed to pay attention to this accounting manipulation until the macro landscape changed.

Yield Up, Price Down

A macroeconomic issue that usually occurs with hot economies began to rear its head again when deposits were flowing into SVB. Inflation grew massively as the U.S. economy, pumped by COVID-19 stimulus, began to overconsume, creating supply and demand imbalances throughout several sectors. The effect was the Federal Reserve’s choice to take decisive action to control skyrocketing price rises by lifting its benchmark rate by 500 basis points (as of the end of March 2023) and conducting the offloading of its balance sheet through quantitative easing. The effect was a rise in yields across the curve that has not been seen in the past decade, as shown in Figure 6.

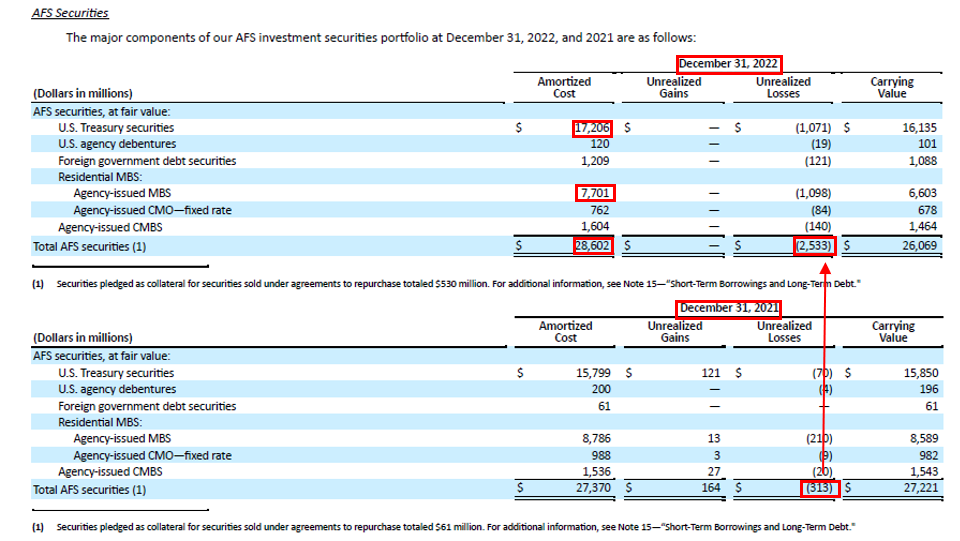

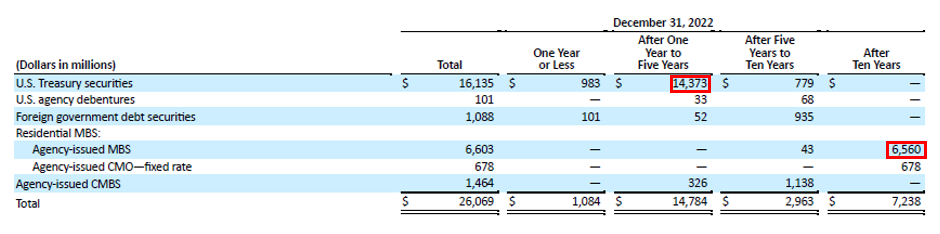

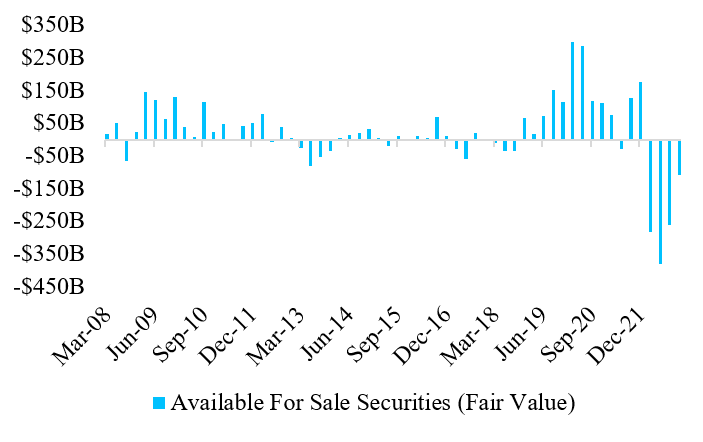

On the asset side, this is when the trouble began for SVB. Thinking about how bond math works, one knows that as rates rise, the pre-existing bonds on the market have their price drop due to better-yielding options becoming available. This is precisely what happened to SVB’s extensive portfolio of AFS and HTM securities, as they were bought when yields were still low. Looking at the AFS side first, one can see that it was a much smaller portion of the overall portfolio sitting at a book value of around $28 billion of the $120 billion. Most of the securities were comprised of Treasuries ($17 billion), with Agency MBS making up the second largest allocation ($7.7 billion). One can also see a relatively sizeable unrealized loss of around $2.5 billion, driven by these securities having both lower yields than the present market offered and having longer maturities in the range of one to five years for the Treasury allocation and over ten years for the MBS allocation. With greater maturity comes more duration, which measures how sensitive a debt security’s price will be to changes in interest rates. The larger duration meant more significant losses on these investments as rates rose. Figures 7 and 8 illustrate the size of the AFS side, the unrealized losses, and the duration it was exposed to.

While a review of the AFS side’s size, duration, and considerable unrealized loss was startling, a glimpse of the larger HTM side is what eventually caused panic. SVB had around $91 billion of the $120 billion portfolio dedicated to the HTM allocation, with a shocking amount of $57 billion in Agency MBS. Worse, most of these MBS had a maturity of over ten years, meaning the duration was substantial, driving the disturbing $15 billion unrealized loss. Figures 9 and 10 display the HTM size, unrealized losses, and maturities.

It is essential to compare the HTM losses to the bank’s capital, which was around $16 billion, as shown in Figure 11.

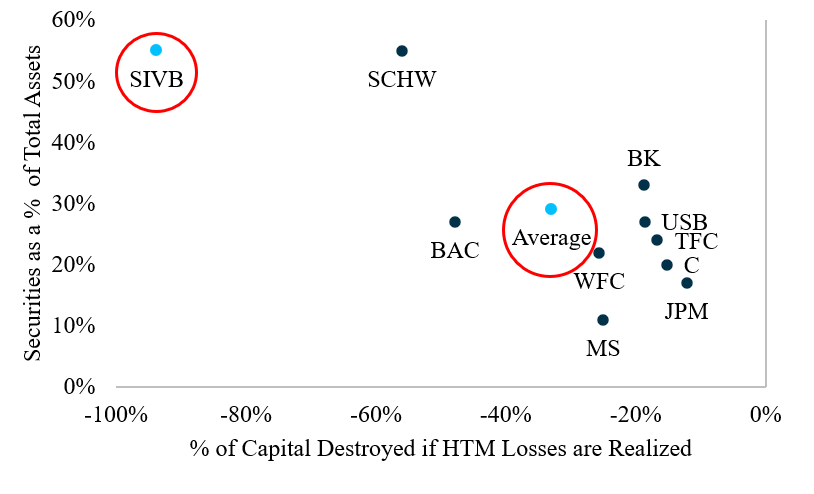

The unrealized losses on the HTM side accounted for 93% of SVB’s capital, which would have been destroyed at any time if the portfolio were to be liquidated in the event of stress. Such a high exposure to losses made SVB stand out as other banks had not committed such a massive portion of their assets to securities. This becomes apparent when one compares the percent of assets in securities, as discussed before, with the unrealized losses as a percentage of capital, as shown in Figure 12.

While SVB is an outlier in how it invested its deposits in longer-duration securities, it exposed a systematic risk that all banks experience as rates rise, which is a decrease in the worth of the ultra-safe assets they hold. For instance, Figure 13 shows the fall in value across the financial sector of institutions with AFS securities. This makes sense, as banks are required to hold these assets to comply with regulations. However, banks also manage risk using financial derivatives such as interest rate swaps to hedge against interest rate exposure. Most banks with large AFS bond portfolios take part in these swaps as an insurance policy; however, when one looks at SVB, it seems they sold off their insurance right before trouble began, which begs the question: why?

Inadequate Risk Management

Interest rate swaps effectively transfer unpreferred types of payments for a preferred type via a switch. For instance, there is a fixed-floating swap that allows the party receiving fixed payments from their investment (think of a traditional bond) to transfer that cash flow to another party that, in return, will pay floating from an asset they hold (think of a Treasury Inflation-Protected Bond (TIP)). There is also floating-fixed, which is just the opposite of the example given above, and floating-floating, where two floating rates are exchanged. The point is that banks like SVB can use these instruments to hedge against changes in interest rates by engaging in a fixed-floating agreement so that as rates rise, they receive a floating rate that adjusts along with them. For HTM securities, the importance of these hedges is diminished since HTM assets are planned to be held until the securities expire. More so, these swaps are also marked at fair value, meaning their volatility with changes in the market will affect the P&L of banks, which is unfavored by most institutions and viewed as not worth the insurance on the HTM side. However, most banks with extensive AFS bond portfolios will engage in these swaps, or instead; they will hold very short-maturity securities such as three-month Treasury bills that have minimal duration. The Financial Times (FT) explains this relationship between the value of swaps and rates concerning the two accounting categories very well:

So if rates rise then a bank makes money on the hedge (receiving a higher floating rate than what it pays in fixed), but the bonds stay at par (if kept in the HTM account). If rates fall then they lose money on the hedge (receiving a lower floating rate than what it pays in fixed), but it can shift bonds from HTM to AFS and sell them at a higher price. That means it basically becomes a directional bet on interest rates that flows straight into the income statement, something most banks abhor. (Wigglesworth, 2023)

While SVB’s duration management was sorely lacking, the bank did seem aware of this issue as they had hedges on their books in early 2021. More so, the bank felt the impending rise of rates the Fed was signaling due to increasing inflation. The CEO, Daniel Beck, addressed that by saying:

…We’re certainly positioning at this point for the potential for higher rates. So in the quarter, we put on close to $10 billion worth of swaps on that available-for-sale portfolio. And we’re going to continue to do more to protect against that, to mitigate the impact of potential further rate movement. (Wigglesworth, 2023)

The company’s financial statements accurately reflect Beck’s promise at the time. However, if one fast-forwards a year, all these swaps seem to have just vanished. By the end of 2022, only $550 million of swaps were left, meaning the rest had been sold, as shown in Figure 14.

Why did SVB take off their insurance? Especially if, at the beginning of 2021, it felt rates would rise. Well, it turns out that as time progressed, rates did rise and began to affect SVB’s clientele of tech startups and VC funds as cheap money no longer existed. The slowdown of the fast-moving startup world was apparent as investors moved away from high cash flow promising growth opportunities to more stable value plays. A great example of this change is shown in Figure 15, showing the number of equity offerings substantially slowing as the Fed signaled and then raised rates throughout 2021 and 2022.

To SVB, this meant fewer deals were available for their clients, and less funding in deposits would flow through the doors. In turn, profitability most likely started to weaken as tech startups needed more of their deposits back (discussed in a later section), there were fewer loans to give out to attractive opportunities, and their bond portfolio was yielding less than the market was giving. These factors resulted in a move to sell their interest rate swaps, leaving SVB open to massive interest rate risk. At the beginning of 2022, SVB started to unwind the derivatives first by selling “$5 billion of AFS hedges to book a $204 million gain, and in the second quarter it dumped another $6 billion of hedges to lock in a $313 million gain” (Wigglesworth, 2023). If one thinks about it, the gains make sense because as rates rise, these hedges become more valuable, meaning they can be sold at a greater price than purchased. However, the point of these hedges was never for speculation but for insurance. SVB seemed to lose sight of that fact in the attempt to sell their protection for a small boost in their profitability to cushion the pain from the macro environment. In simpler terms, the bank sold its protection for a small gain in exchange for exposing itself to the probability of significant losses that materialized. Management suggested that these sales were part of a transition to focusing on “downrate sensitivity” (Wigglesworth, 2023). The company was essentially attempting to call the peak in interest rates while cushioning its profitability. Curiously, management was sort of right in that rates on the long-end 10-year Treasury peaked at around 4.25% in October of 2022. However, this did not prevent the rise in unrealized losses nor the equity investors or depositors from noticing. Once they did, the lack of insurance was not there to protect the bank from the spark that caused the institution's failure.

A Concentrated, Shrinking Funding Base

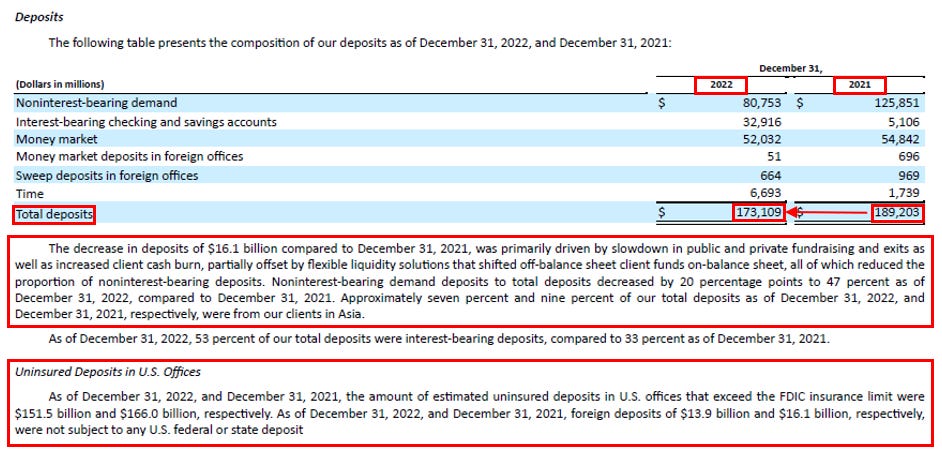

The heavily concentrated depositors that made up the liability side of SVB’s balance sheet felt the effects of the changing macro environment the most. As rates rose, money became more expensive, causing deals to slow and startups to burn through cash quicker. This caused a need for their deposits which the bank had to hand over. Another critical point is that most of SVB’s depositors were businesses instead of consumers. This matters because as rates rise, companies are more willing to move their deposits to a higher yielding option, such as a money market mutual fund, instead of a bank that is holding deposit rates low to keep net interest margins (NIM) level (NIM is just a bank’s returns from its assets minus what it pays its depositors or to its debt holders). With rising rates, SVB’s NIM was shrinking as its cost to keep depositors increased. For instance, “in the fourth quarter of 2021, its cost of deposits rose 2.33 percent, from 0.14 percent in the final quarter of 2021. That’s bad but not lethal: the company’s interest-bearing assets yielded 3.36 percent in the fourth quarter, up from 1.99 percent, rendering a tightening (shrinking profitability) but still positive spread” (Armstrong, 2023). These combined factors made deposits slip; by the end of 2022, they decreased by $16.1 billion. However, this fall was not the most dangerous thing about SVB’s funding base. If one looked at the percentage of uninsured deposits, it could be seen that almost 88% were above the $250,000 protection the Federal Deposit Insurance Corporation (FDIC) promises to back up if a bank fails. This is extremely important as it incentivized a large portion of SVB’s funding base to flee if any trouble was suspected, as businesses knew they most likely would not get their money back if the bank fell. The breakdown of these deposits is shown in Figure 16.

Lighting the Tinder Box

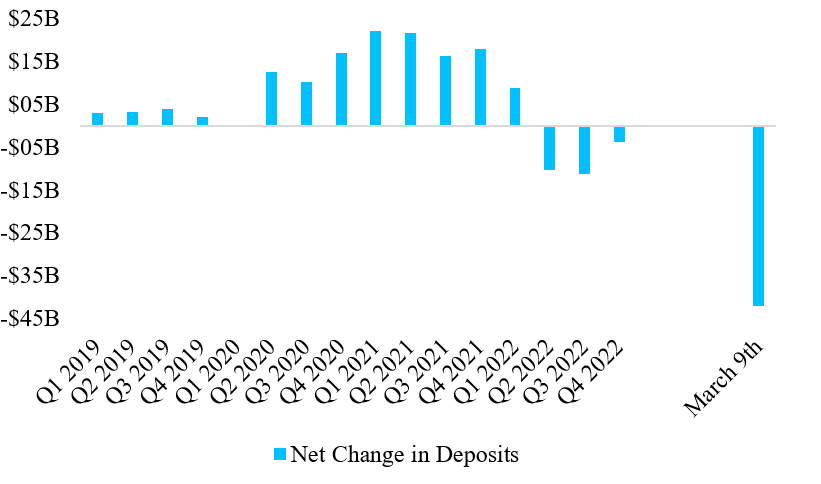

As 2023 emerged, the bank most likely realized that deposit bleeding might continue and that profitability could suffer further. To remedy this, SVB attempted to switch some of its longer-duration assets in the bond portfolio with shorter-duration, higher-yielding investments. The decision to do so resulted in almost all of the AFS securities being sold to the larger investment bank, Goldman Sachs. Due to the sale, SVB was forced to record a $1.8 billion loss, and to patch that hole in its capital; it decided to work with Goldman Sachs to raise new equity in the amount of $2.25 billion. The choice by the bank to rearrange its portfolio sparked major concern from depositors and investors, who decided to take a closer look at the company’s financials. Once it was discovered that SVB had unrealized losses on its HTM securities of almost all of the company’s equity, panic ensued, and the dominoes began to fall. SVB rushed to meet withdrawals from depositors as equity investors sold stock as fast as possible. The bank encountered several obstacles while trying to stop the bleeding. The equity offering run by Goldman Sachs fell through as investors realized a run on the bank was materializing. Some may also argue that the equity offering would never have worked due to the lack of confidence behind Goldman Sachs, which never actually underwrote the deal. On the depositor side, SVB quickly found itself running out of cash and realized it would have to either sell its HTM assets or use them as collateral to acquire funding from lenders of last resort. The latter option was much preferred; however, as Wall Street Journal (WSJ) points out that on Thursday, March 9th, the day the bank was experiencing its highest withdrawals and was attempting to borrow the cash, it ran out of time as the computers that process the transactions at the Fed close at 4:00 p.m. PT and do not open until the next day. The WSJ writes, “The Fed needed a test trade to be run before the actual transfer could occur. That took time and the Fed didn’t extend its own daily deadline of 4:00 p.m. PT for collateral transfers to help SVB. Time ran out on the bankers and SVB couldn’t get the money that day” (Miao et al., 2023). As a result, the bank could not acquire enough funding to stop the run and, on that Thursday, suffered deposit outflows of $42 billion, as shown in Figure 17.

The following day, Friday, March 10th, it was announced:

Silicon Valley Bank, Santa Clara, California, was closed today by the California Department of Financial Protection and Innovation, which appointed the Federal Deposit Insurance Corporation (FDIC) as receiver … All insured depositors will have full access to their insured deposits no later than Money morning, March 13, 2023. The FDIC will pay uninsured depositors an advance dividend within the next week. Uninsured depositors will receive a receivership certificate for the remaining amount of their uninsured funds. (Scaggs, 2023b)

Government Intervention

The decision by the FDIC to take SVB into receivership and insure both insured and uninsured depositors effectively ended the bank’s 40-year history. The government’s choice to save SVB has been met with several viewpoints as discussions about moral hazard and too interconnected to fail clash. On the one hand, moral hazard has its place in this discussion as the poor choices by the management of SVB, which resulted in its failure, were quickly remedied by government intervention. However, it is vital to remember that in the event of bankruptcy, which the company entered on March 17th (a little over a week after the initial crisis), equity investors usually get next to nothing while management is fired, and creditors obtain anything left from the sale of assets. More so, management is usually given a certain amount of company shares as a part of their compensation package, meaning they suffer heavily when the business they run goes under. In effect, management is punished by the loss of their jobs, equity, and credibility, while investors lose capital due to poor due diligence. On the other side, the government’s backing of depositors of both insured and uninsured nature adheres to the argument that SVB was too interconnected with the venture capital community to fail. A stronger argument for this would center around the psychology between humans and banking, where confidence is key. If the government had just let SVB fall, panic might have spread further and wider than the initial fear the bank’s failure caused. The backing by the government ensured that other liquid and solvent banks with proper risk management were not punished with unnecessary bank runs. That being said, the result of SVB’s failure has already dealt confidence damage that cannot be undone. It will most likely result in the increased cost of funding for banks as jittery depositors move their funds to either super large banks deemed too big to fail or to money market accounts yielding close to five percent (as of March 2023). Due to this, banks will most likely see a shrinking of NIM as profitability is squeezed from both the liability and asset side via tightening lending standards to keep a more significant amount of capital in case of deposit outflows. The result could trickle throughout the U.S. economy as lending slows, causing businesses and consumers to borrow less as it becomes more expensive. However, only time will tell if these issues materialize.

Conclusion

The fall of Silicon Valley Bank exposed systematic interest rate risk that all banks experience in a rising rate environment. As mentioned, most of these banks work to protect against these risks via shorter maturity assets or interest rate swaps. SVB did not. Through several individual choices made by the bank’s management, it exposed itself to unnecessary danger in exchange for short-term profitability that eventually resulted in its downfall. As a result, the FDIC took SVB into receivership before ultimately selling the company’s assets to First Citizens Bank. The story of SVB’s failure is one of the ever-growing importance of risk management within a financial institution. More so, SVB’s case emphasizes the importance of seeing beyond short-term profits to consider long-term threats that can destroy over 40 years of development.

Note from Author

Hi everyone, I apologize for the length; there are multiple narratives that weave together with this story and I felt it was important to include them all. As always, I hope you enjoyed reading as I enjoyed writing! If you want to learn more, I have included both an annotated bibliography and works cited below that displays the sources used for this piece.

Annotated Bibliography

Armstrong, R. (2023, March 10). SVB is not a canary in the banking coal mine. Financial Times. https://www.ft.com/content/7cf4eb45-78b7-4e6e-b134-1f0b082ba203

Robert Armstrong runs Unhedged, offered by the Financial Times. He writes market commentary with his co-author, Ethan Wu, almost every day. When Silicon Valley Bank failed, Armstrong and Wu wrote several pieces detailing different aspects of the bank's failure. This article is an excellent example as Armstrong makes several points about the individual risks and characteristics that made SVB's failure self-induced and not a signal for banks everywhere being in danger of suddenly failing.

Dodd-Frank Act. (2018, August 21). History.com. https://www.history.com/topics/21st-century/dodd-frank-act

The Dodd-Frank Act was instituted in 2010 by the Obama administration. It was created to enforce heavier regulations and supervision on banks with assets over $50 billion. This held until 2018 when the Trump administration changed the law to allow banks with assets under $250 billion to have less scrutinizing enforcement compared to their larger colleagues. This article by History.com lays out the details behind the original Dodd-Frank Act.

FDIC | Failed Bank List. (n.d.). https://www.fdic.gov/resources/resolutions/bank-failures/failed-bank-list/

The Federal Deposit Insurance Corporation (FDIC) frequently releases U.S. bank data. In this example, the FDIC shows the number of failed banks with their size in both assets and deposits. One can examine that Silicon Valley Bank is second to the top of the list as Washington Mutual Bank, which failed in the 2008 financial crisis, was the largest bank to go under in U.S. history.

Ferguson, N. (2008). The Ascent of Money: A Financial History of the World: 10th Anniversary Edition. Penguin.

Niall Ferguson's The Ascent of Money is a detailed book describing the history behind the creation of money and its ability to improve economies throughout the globe. Ferguson instructs readers in the creation of debt, equity, insurance, housing, and other critical financial topics that exist in the world today. Ferguson also gives an account of the 2008 financial crisis, which occurred while writing the book, with a brief mention of the Dodd-Frank Act, which was seen as a rush to regulation by lawmakers after the spread of banking contagion.

Levine, M. (2023, March 22). Silicon Valley Bank Ran Out of Money. Bloomberg.com. https://www.bloomberg.com/opinion/articles/2023-03-22/silicon-valley-bank-ran-out-of-money#xj4y7vzkg

Matt Levine writes for Bloomberg Opinion and focuses on several topics within the finance world. His past experiences include being an editor of Dealbreaker, an investment banker at Goldman Sachs, and a mergers and acquisitions lawyer at Wachtell, Lipton, Rosen, and Kratz. Levine is a highly talented and knowledgeable writer that followed the failure of Silicon Valley Bank as it occurred. He brought several fine points to the table, including the highlighting that SVB ran out of money due to the computer that processes transactions through the Federal Reserve closing at 4:00 pm PT, which was first revealed by the Wall Street Journal (article quoted within the paper).

Parlapiano, A., Solomon, D. B., Ngo, M., & Cowley, S. (2022, March 12). Where $5 Trillion in Pandemic Stimulus Money Went. The New York Times. https://www.nytimes.com/interactive/2022/03/11/us/how-covid-stimulus-money-was-spent.html

This New York Times article lays out the total amount of Covid stimulus the government provided in stunning detail. It breaks down where these funds went, such as households and businesses. The effects of this stimulus were apparent for Silicon Valley Bank as the cheap money that flowed throughout the economy gave markets a boost resulting in more equity deals being completed. In turn, SVB's clients of startups had more cash which they parked within the bank.

Peccatiello, A. (2023a, March 12). Banking Crisis? By Alfonso Peccatiello (Alf). https://themacrocompass.substack.com/p/banking-crisis

Alfonso Peccatiello writes a personal substack commentary named The Macro Compass, where he addresses macro events occurring throughout the world and the best way he feels to trade them. Peccatiello has managed money and has significant experience addressing macroeconomic changes and how they affect markets. This article discusses the failure of Silicon Valley Bank and some of the individual risks the bank took that ultimately led to its demise.

Scaggs, A. (2023a, March 9). Silicon Valley Tank(s). Financial Times. https://www.ft.com/content/c94279a4-4ec2-4a0c-86fb-be8375e12ef2

Alexandra Scaggs writes for the Financial Times and provided several excellent articles about the failure of Silicon Valley Bank as it occurred. This article discusses the fall in SVB's stock price as panic ensued before the bank's demise. Another report by Scaggs quoted within the paper discusses SVB being taken into receivership by the FDIC, which occurred on March 10th, a day after this article was written.

The Harvard Law School Forum on Corporate Governance. (2018, June 13). Rolling Back the Dodd-Frank Reforms. https://corpgov.law.harvard.edu/2018/06/13/rolling-back-the-dodd-frank-reforms/

This article by Harvard Law described the legislation change to the Dodd-Frank Act that occurred in 2018 under the Trump administration. The easing of the Act created an environment where smaller banks of assets under $250 billion, such as Silicon Valley Bank, could operate with less regulation and supervision. More specifically, the stress tests and balance sheet risk-taking restrictions were more relaxed than larger banks within the United States.

Wigglesworth, R. (2023, March 17). How crazy was Silicon Valley Bank’s zero-hedge strategy? Financial Times. https://www.ft.com/content/f9a3adce-1559-4f66-b172-cd45a9fa09d6

Robin Wigglesworth, via the Financial Times, writes this excellent article detailing in easy-to-understand how the elimination of hedging occurred within Silicon Valley Bank. Wigglesworth breaks down the relationship between interest rate swaps, accounting measures, and interest rates changing in the macroenvironment. He also displays the elimination of these swaps via SVB's 10-K. More so, he describes how combined with no hedging, SVB's liability side was highly concentrated and interconnected, eventually leading to quicker panic when the trouble started.

Works Cited

Armstrong, R. (2023, March 10). SVB is not a canary in the banking coal mine. Financial Times. https://www.ft.com/content/7cf4eb45-78b7-4e6e-b134-1f0b082ba203

Bloomberg L.P. (n.d.). Bloomberg [Dataset]. https://www.bloomberg.com/professional/solution/bloomberg-terminal/

Ferguson, N. (2008). The Ascent of Money: A Financial History of the World: 10th Anniversary Edition. Penguin.

Goswami, R. (2023, March 13). Silicon Valley Bank signed exclusive banking deals with some clients, leaving them unable to diversify. CNBC. https://www.cnbc.com/2023/03/12/silicon-valley-bank-signed-exclusive-banking-deals-with-some-clients.html

Miao, H., Zuckerman, G., & Eisen, B. (2023, March 22). How the Last-Ditch Effort to Save Silicon Valley Bank Failed. WSJ. https://www.wsj.com/articles/how-the-last-ditch-effort-to-save-silicon-valley-bank-failed-89619cb2

Parlapiano, A., Solomon, D. B., Ngo, M., & Cowley, S. (2022, March 12). Where $5 Trillion in Pandemic Stimulus Money Went. The New York Times. https://www.nytimes.com/interactive/2022/03/11/us/how-covid-stimulus-money-was-spent.html

Peccatiello, A. (2023a, March 12). Banking Crisis? By Alfonso Peccatiello (Alf). https://themacrocompass.substack.com/p/banking-crisis

Peccatiello, A. (2023b, March 14). Contagion Risks. By Alfonso Peccatiello (Alf). https://themacrocompass.substack.com/p/contagion-risks

Rosenthal, J., Simon, P., & Milonopoulos, G. (2023, March 10). U.S. Banks: SVB Situation More “SV” Than “B.” CreditSights.

Santilli, P., & Benedict, J. (2023, March 12). Silicon Valley Bank’s Meltdown Visualized. WSJ. https://wsj.com/articles/silicon-valley-banks-meltdown-visualized-3da2263b?mod=saved_content

Scaggs, A. (2023b, March 10). SVB: RIP. Financial Times. https://www.ft.com/content/cea7e32a-5ea3-4a6f-ab6d-1360a9de9557

Silicon Valley Bank. (n.d.). Silicon Valley Bank. https://www.svb.com/newsroom/facts-at-a-glance

SVB Financial Group - Financials - SEC Filings. (n.d.). https://ir.svb.com/financials/sec-filings/default.aspx

The Harvard Law School Forum on Corporate Governance. (2018, June 13). Rolling Back the Dodd-Frank Reforms. https://corpgov.law.harvard.edu/2018/06/13/rolling-back-the-dodd-frank-reforms/

Wigglesworth, R. (2023, March 17). How crazy was Silicon Valley Bank’s zero-hedge strategy? Financial Times. https://www.ft.com/content/f9a3adce-1559-4f66-b172-cd45a9fa09d6