Why are Companies Staying Private Longer?

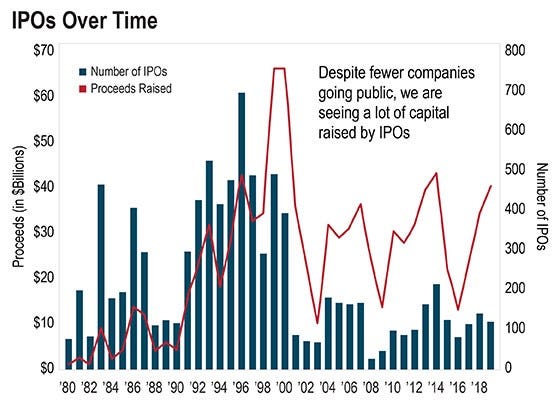

Initial public offerings (IPOs) sharply declined after the dot-com bubble burst, never recovering to pre-bubble levels. Inversely, the funds raised through IPOs each year has been disproportionately higher than the number of IPOs per year, indicating that companies need more investment capital than ever before to compete in today’s corporate environment (Figure 1 displays this relationship).

Although the public market appears more than capable of accommodating the companies that choose to IPO, the falling number of IPOs each year begs the question: “how are big companies that are not IPOing meeting their needs for capital?” The answer is that they are staying private longer, and raising what are referred to as private “mega-rounds.” Mega-rounds are defined as private financing rounds in which companies raise more than $100 million. Shockingly, as Figure 2 shows, these mega-rounds eclipsed tech IPOs in deal number long ago in 2013 and have since skyrocketed.

IPOs as a whole still contribute far more capital to companies than mega-rounds do, demonstrating that there is still a significant need for IPOs. However, the fact remains that an unprecedented amount of companies that could IPO are choosing not to. Why?

The reason as to why more companies are staying private is widely debated, but it is somewhat of a chicken-and-egg issue. It is hard to discern which came first: the private equity industry expanding and being able to accommodate larger capital requirements (eliminating the need to IPO for many companies) or IPOs declining due to entrepreneurs trying to avoid a number of challenges associated with them (presenting the private equity industry the increased demand it needed to expand to finance larger rounds). However, it is widely agreed upon that regardless of how this phenomenon came to be, the many advantages of staying private are what drives a company to wait longer to IPO.

Here are just a few of the factors that drive a company to stay private longer:

Going public is often the time for private investors (and sometimes, company executives) to cash out, and for new public investors to take their place. Many entrepreneurs would prefer not to engage with new shareholders who might take their company in a different direction than they intended, especially since in the public market the entrepreneur has no control over who their shareholders are. In addition, going public typically dilutes a founder’s ownership in their company, exacerbating their decrease in control. Staying private longer can temporarily avoid this issue.

Many founders also prefer to execute long-term growth strategies in the private market where there is less pressure from Wall Street analysts, rather than focusing on short-term quarterly earnings as the public market encourages.

When a company goes public, its financials become public too and it loses the advantage of having this information shielded from competitors’ eyes. Disclosure requirements are minimal for private companies, incentivizing many companies to remain private to retain the advantage of its financials and other vital information remaining undisclosed to the public.

With the exception of a few large private companies, public companies generally face more public scrutiny than private ones do. Additionally, staying private protects a company from other risks including activist investors, hostile takeovers, and shareholder lawsuits.

As share price in the public market is determined by supply and demand, a company’s valuation becomes much more volatile once it goes public. For this reason, IPO timing is crucial. If the market suffers significant losses or negative changes in investor sentiment prior to a company’s IPO, the company can suffer an immense valuation drop upon IPO. Many companies never recover from such valuation plummets. Staying private avoids this risk, and the ongoing market volatility risk that going public entails.

The significant costs to IPOing alone can be enough to encourage companies to stay private longer. According to the American Bar Association (ABA): “The average cost of completing an IPO has been estimated to be approximately $4 million, on top of an average one-time fee of $1 million to prepare the organization to become a public company and the recurring average $1.5 million annually to comply with ongoing regulations.”

The US Jumpstart Our Business Startups (JOBS) Act increased the maximum amount of shareholders a company can have before it must publicly disclose its financial statements from 500 to 2,000. This change allows companies to stay private longer before they must comply with SEC public reporting requirements without in fact becoming a publicly traded company and reaping the benefits associated with going public. The prior limit of 500 shareholders, in effect, forced many companies (such as Google) to go public to avoid having to meet the disclosure requirements without also benefiting from being publicly traded.

Ultimately, many companies are staying private longer simply because they can. The global private market’s funds now amount to over $750 billion. As such, the private equity industry has become increasingly capable of providing the large investment amounts that many companies could only have obtained from IPO underwriters a decade or two ago. As is shown in Figure 3, mega-rounds have gone from being relatively rare anomalies to being fairly common.

For better or worse, companies are responding to incentives to stay private by doing just that. Today, the average time from company inception to IPO is 11 years, up from a 7 year average in 2010.

All great points as always Jason! US VC-backed tech exits are definitely creeping up slowly since 2014, but still far below the dot com bubble as you noted. Median equity raised at and prior to IPO is also at a ten-year high! Check our latest State of the Markets: (https://www.svb.com/globalassets/library/uploadedfiles/svb-q1-2021-state-of-the-markets-report2.pdf)

Some other themes worth noting:

1) The onset of SPACs as a liquidity option with a far lower cost of capital than traditional IPOs and the SEC approval of Direct Listings with capital raises. Taking these into account skews the IPO statistic a bit but probably provides a more accurate picture of what's going on.

2) One of the "why's" of the massive growth of PE/VC dry powder. Our low interest rate environment is driving traditional and non-traditional private investors to seek yield wherever possible. LPs are increasing their % of AUM allocation in PE/VC to accommodate. As you mentioned, more demand for private company stock is creating less pressure to raise from public markets.

3) Soon (maybe) liquidity will get a lot easier for private shareholders and further decrease the urgency to IPO. Check out what's going on with CartaX, NASDAQ, and other companies trying to build private stock exchanges. Also less discussed, but employees can suffer too from lack of liquidity. Products like AngelList's new Recurring Liquidity service could change this problem for the better.

4) Dual-class shares and their impact on founder control post-IPO. FB, Doordash, Snap, Palantir, Spotify, etc. are all part of the new wave of tech CEO's getting way more votes per share than you typically see (For better or for worse). Something that was maybe non-negotiable in the past might soon be a standard and change the control equation.

Great work!